On 14th April Elon Musk announced a hostile take-over of Twitter, offering a cash deal valued at $43 billion to take the company private. In this 7investing article, lead advisor Luke Hallard shares his views on the recent news cycle, and why there are likely to be very few good outcomes for Twitter shareholders over the coming weeks while the boardroom drama plays out.

April 14, 2022

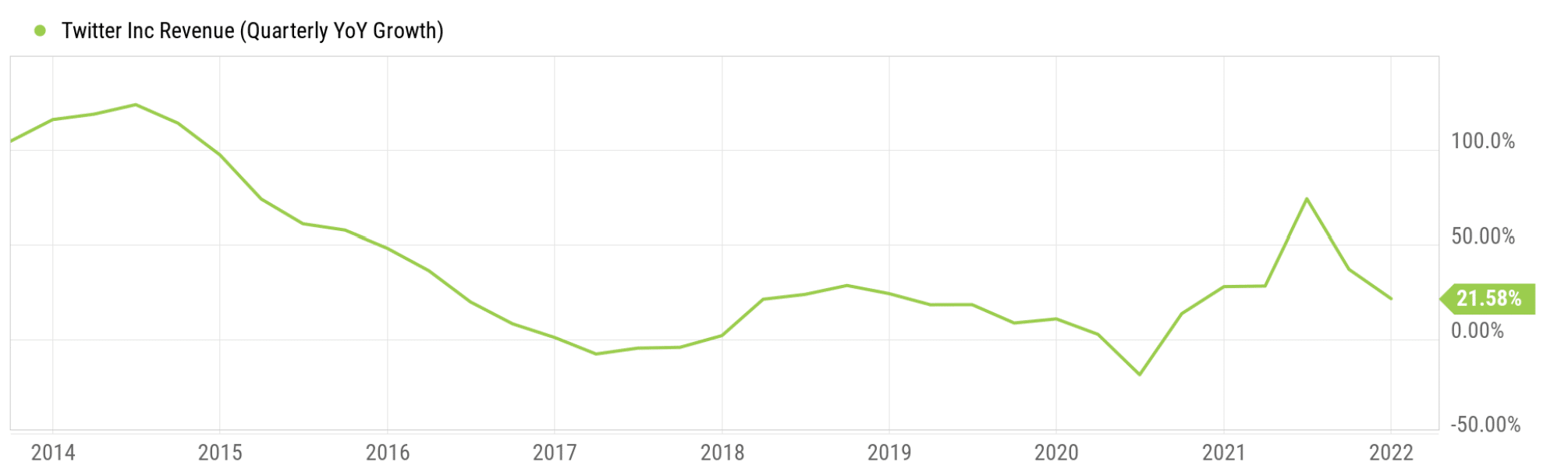

Wow, these last few weeks have been a hot mess for Twitter’s (NYSE: TWTR) board of directors, and once again billionaire businessman Elon Musk is in the spotlight.

In early April, it was revealed (somewhat late, which has resulted in a class-action lawsuit from investors) that Musk has been quietly accumulating shares in the company since late January, becoming the largest individual shareholder. While buying up stock, Musk has used his influence with his 81 million followers on the platform to openly criticise the company in a series of tweets questioning whether Twitter supports the principles of free speech, whether the algorithm is biased, and even suggesting that a replacement might be needed.

Perhaps seeking some control over the narrative, on 5th April, Twitter’s board, led by CEO Parag Agrawal, invited Elon to take up a governance role at the company, but just four days later Musk announced that he would be declining the offer – likely deterred by his board member obligation to act in the best interests of the company – an obligation that might perhaps tie his hands with the nature of the changes that he actually wants to effect.

This morning, Elon announced a hostile take-over, offering a cash deal valued at $43 billion to take Twitter private. His announcement is an egg on the face for Twitter’s board, and the terms of his offer specifically state a lack of confidence in management. It’s currently unclear whether the board will accept the offer, make a counter-offer, seek to solicit other bids, or simply decline and seek to continue as a public company – but however things shake out, there are likely to be few good outcomes for Twitter shareholders.

If Elon’s offer letter is to be taken at face value, there will be no further negotiation on the acquisition price. Unless the market believes that Musk has shone a light on Twitter’s hidden value, his offer of $43 billion is likely to set a ceiling on the share price in the immediate term. If the offer falls through or is declined by the board, Musk’s criticism is likely to prove fatal to Agrawal, who only took up the CEO role five months ago, and is likely to cause further damage to Twitter’s valuation.

A side effect of recent headlines has been the news that “super stressed” Twitter employees are granted a monthly ‘day of rest’ – a drain on productivity, but more importantly a clear indictment of company culture that a benefit of this nature is required. I imagine this isn’t the last ugly headline that investors are likely to see before this news cycles runs its course.

Elon has been quoted as saying that “the most entertaining outcome is the most likely”, but he’s indisputably an extremely smart businessman. While there can be little doubt that his actions have created rather good entertainment for himself (he tweeted and then deleted a rather sarcastic emoji in response to Agrawal’s board announcement), there are also several potential business benefits to his actions of the past few months.

And of course while it’s certainly not material to the business case for acquisition, it probably hasn’t escaped Musk’s attention that he’ll suddenly be the owner of what is arguably the world’s biggest news outlet, rather putting space-race competitor Jeff Bezos’ ownership of The Washington Post in the shade…

I’ll be watching how things play out over the coming days with some interest, but my own journey as a Twitter shareholder came to an end today and I’ve exited a personal stock position that I’ve built up fairly steadily since 2013. I don’t anticipate significant upside beyond the $43 billion offer, and there would seem to be a material downside risk, at least in the short to medium term while the company re-stabilises, if it even continues as a public market investment.

If there’s any small consolation to this very messy situation, I guess Block (NASDAQ: SQ) shareholders can perhaps breathe a sigh of relief that Twitter founder Jack Dorsey has built some distance from the company, so likely won’t be pulled directly into trying to steady the ship, wherever we go from here.

Already a 7investing member? Log in here.