In a surprising turn of events, 7investing is selling its entire stake of Celsius Holdings.

Companies: Celsius Holdings

I know. This is quite an unusual sell recommendation to write.

I made Celsius Holdings (Nasdaq: CELH) my official recommendation just eleven days ago. And yet today, less than two weeks later, 7investing is selling it entirely from our scorecard.

If this is surprising to you, I’ll admit that it’s surprising to me too. I was enamored with the company’s incredible growth, its excellent margins, and its international expansion. I recorded podcasts and Spaces episodes as recently as this week describing how bullish I was about the stock and the company’s future. This year’s selloff felt like a perfect opportunity to buy a real winner while it was selling at a bargain.

But then it all hit me.

It was like the feeling of being unable to look away from a terrible car crash, coupled with realizing you’d just eaten expired lunch meat. I got a grotesque, regretful feeling in the pit of my stomach that I simply couldn’t shake off.

And the more I read, the more red flags I kept finding. The further I went down the rabbit hole, the yuckier the gut feeling became.

Celsius was beginning to feel more like a marketing hustle than a sustainable compounder of capital.

After much internal debate, I realized that Celsius is not the company that I thought it was and it also is not the type of company I want to recommend for 7investing.

This is a mea culpa event. But it’s also the right decision.

So after an unusual combination of remorseful, objective, and investigative research, 7investing will be selling all shares of Celsius Holdings from our scorecard.

Now, let’s jump to the chase. Here are the seven red flags — all of which I discovered just yesterday — that ultimately led me to this decision.

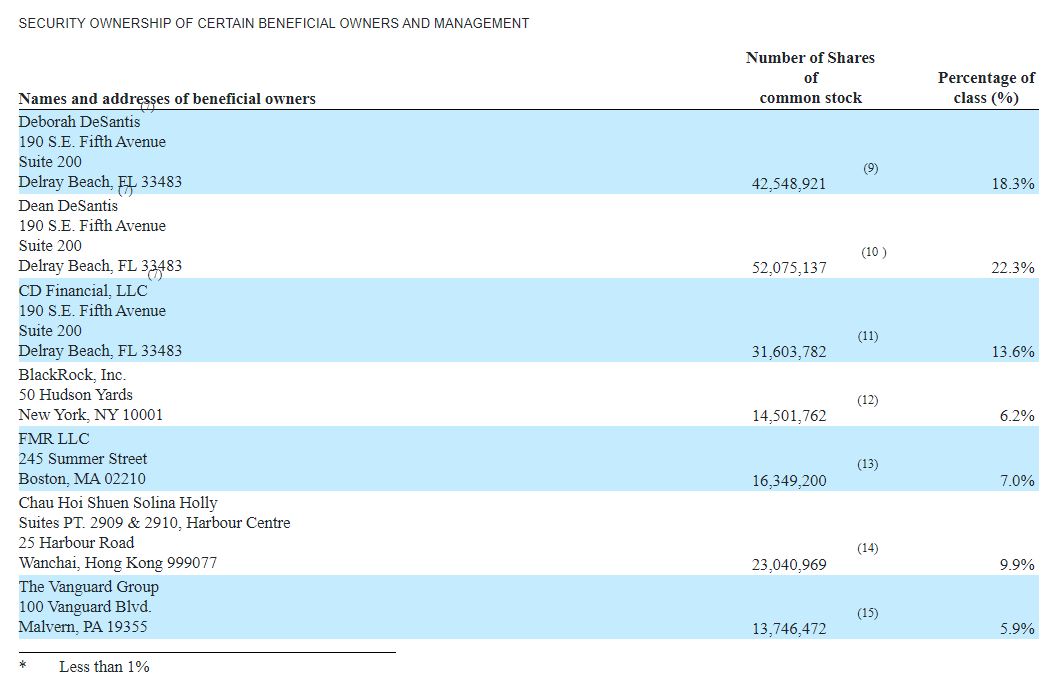

Note: this section has been updated. It was previously reported that Carl DeSantis and his family trust funds owned 54% of Celsius. Due to overlap between multiple funds, the actual ownership of the family is closer to 22.8%. These numbers have been adjusted below.

If we go back in time twenty years, Celsius’ earliest investor was the billionaire entrepreneur Carl DeSantis.

DeSantis was a lifelong hustler; a serial entrepreneur who ran businesses that ranged from parakeet breeding to operating a drugstore to manufacturing his own line of sunscreen. His biggest success was founding a vitamin and nutritional supplement company called Rexall Sundown, which eventually got acquired for $1.8 billion.

DeSantis saw promise in Celsius’ health claims. When the company was financially struggling, it was he who brought in John Fieldly (who is currently CEO and Chairman) to right the ship by relisting Celsius on the Nasdaq. His goal in doing that was so “insiders could get their investment back.”

As of last summer, Carl was the single-largest individual owner of Celsius, which was worth nearly $16 billion as an enterprise at the time.

Carl DeSantis then unfortunately passed away in August 2023 and he left his entire fortune to his family.

Directly following his death:

Altogether, those ownership stakes add up to 22.8%.

Even though Celsius is a multi-billion dollar and soon-to-be international business, it is still largely owned by the three surviving members of the DeSantis family. That’s a huge ownership concentration risk.

Source: 2024 Proxy Statement (page 8)

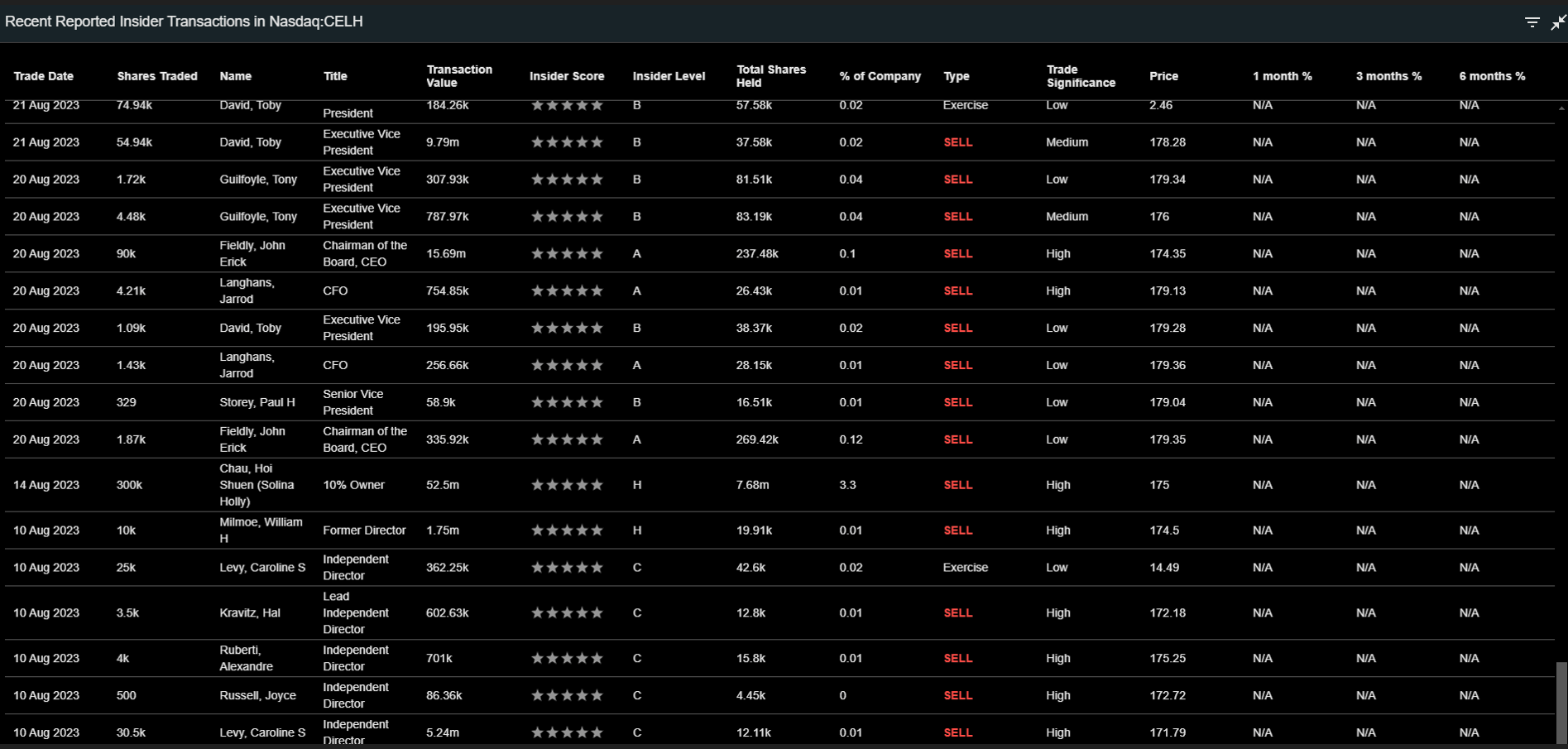

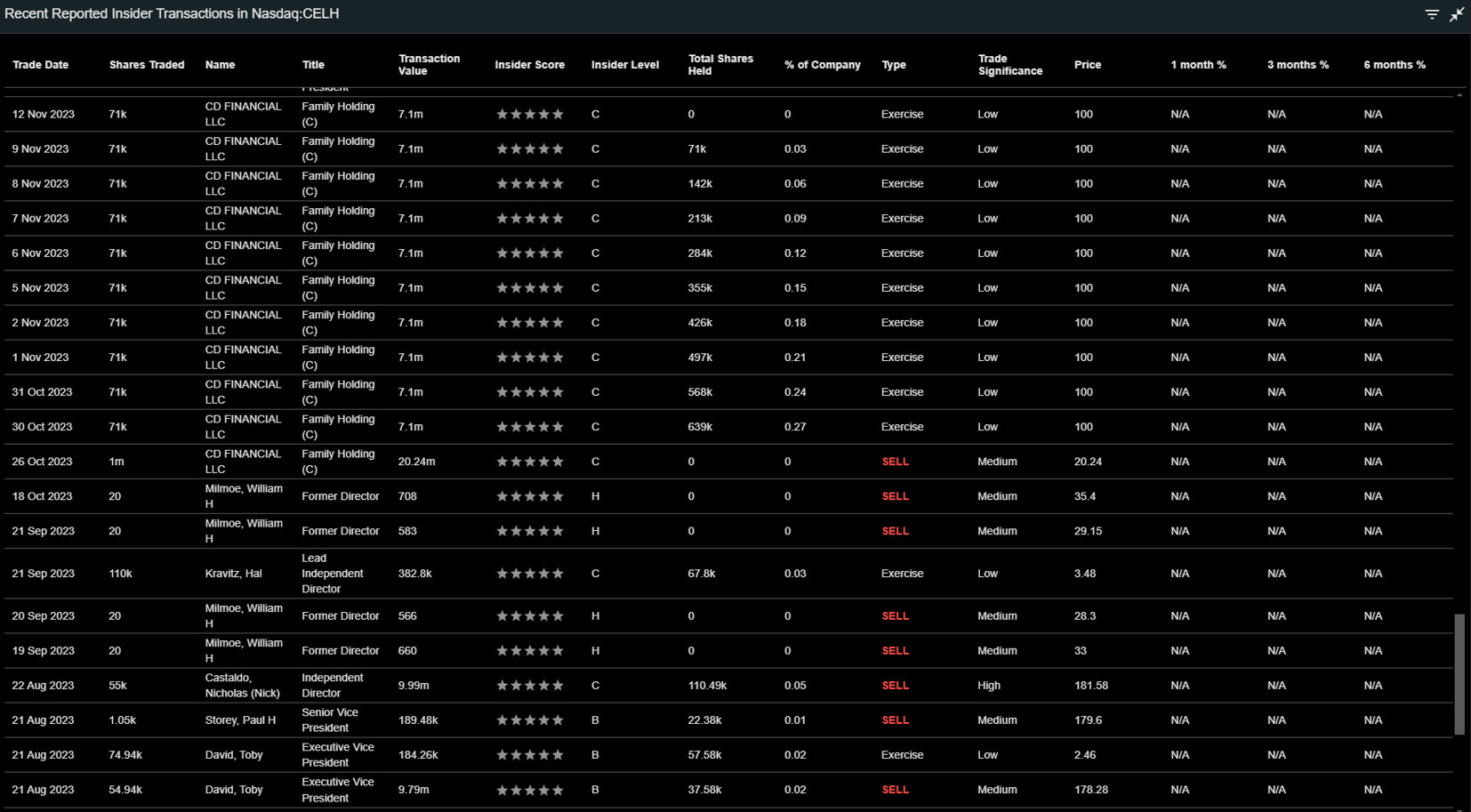

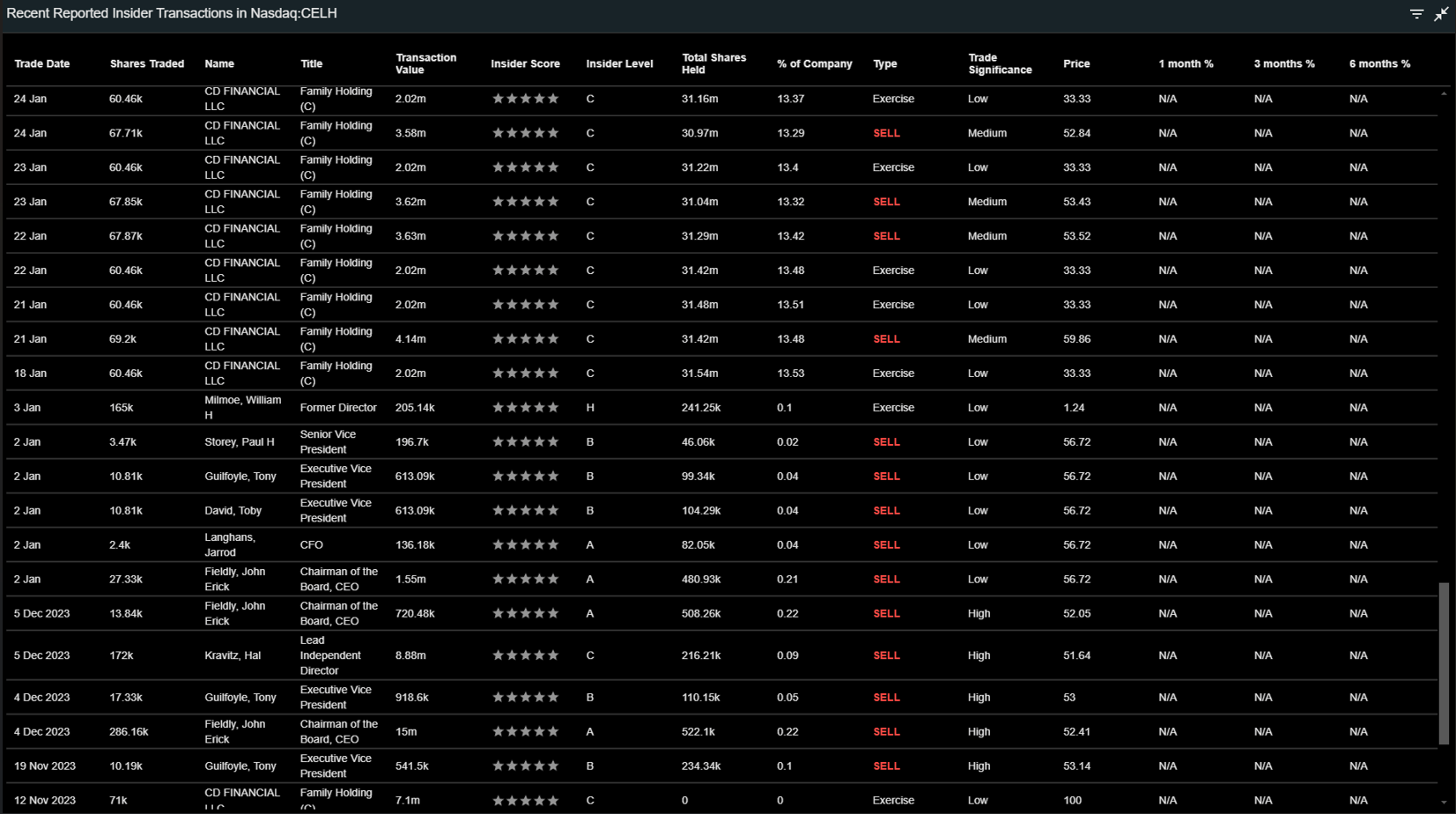

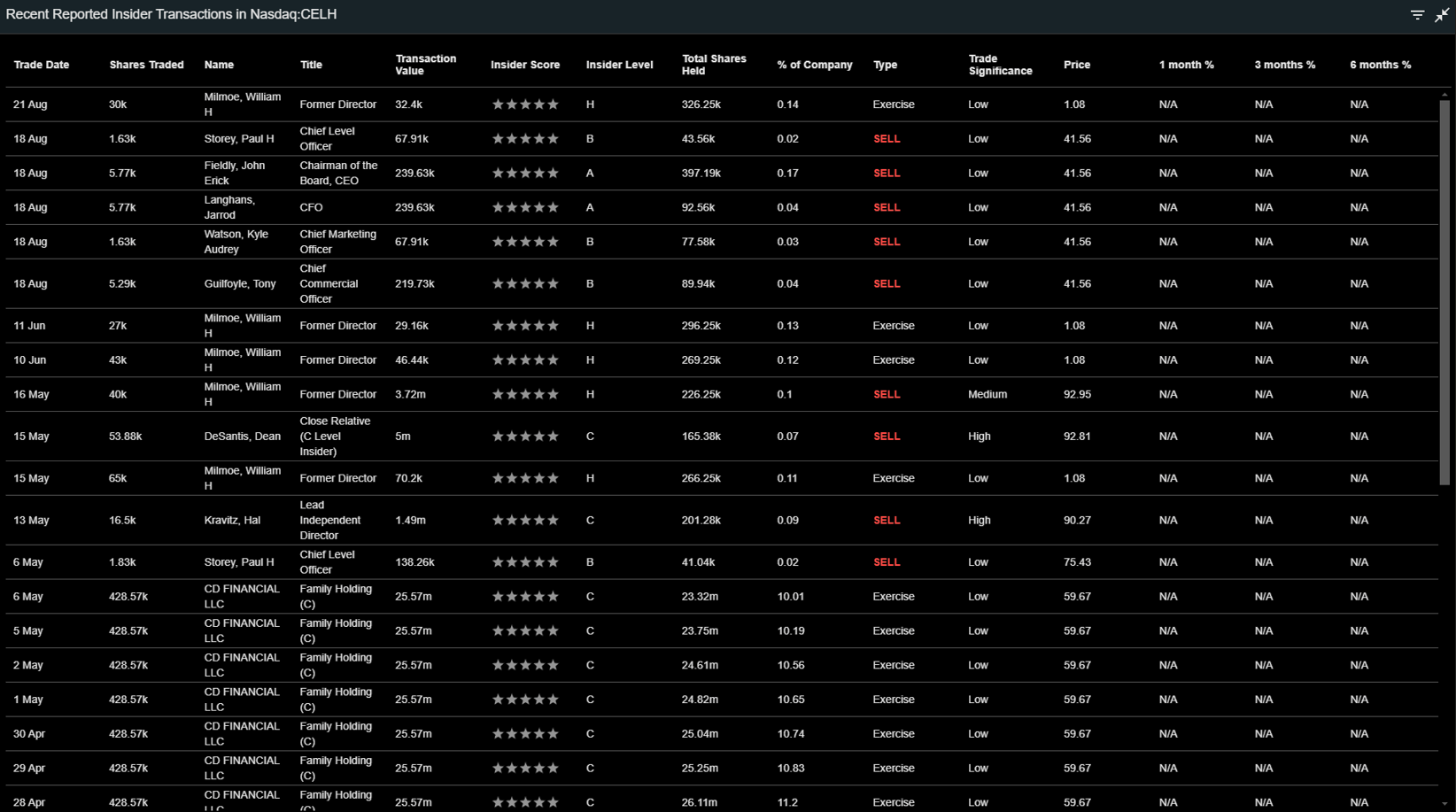

Yet directly following Carl’s death on August 10, 2023, his family almost immediately began cashing out their shares.

In the twelve months since Carl DeSantis died:

The DeSantis family has not bought any new shares of Celsius.

It’s very unclear what their motivation is going forward, in terms of whether they intend to hold or to sell their remaining positions. No one in the family has had an operational role in the business, except for Damon who sits on the Board of Directors.

Celsius lists seven executive managers on its leadership team. They are:

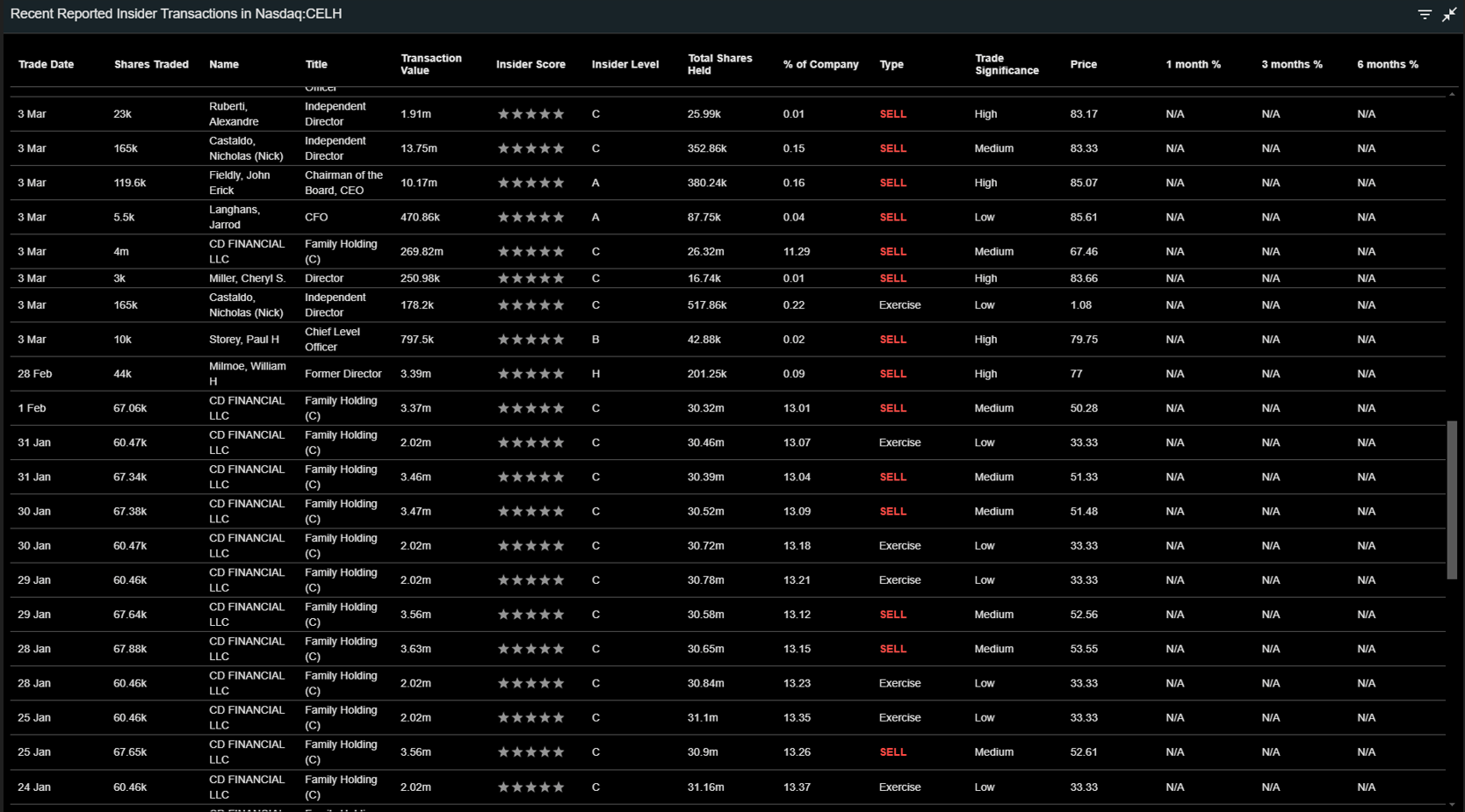

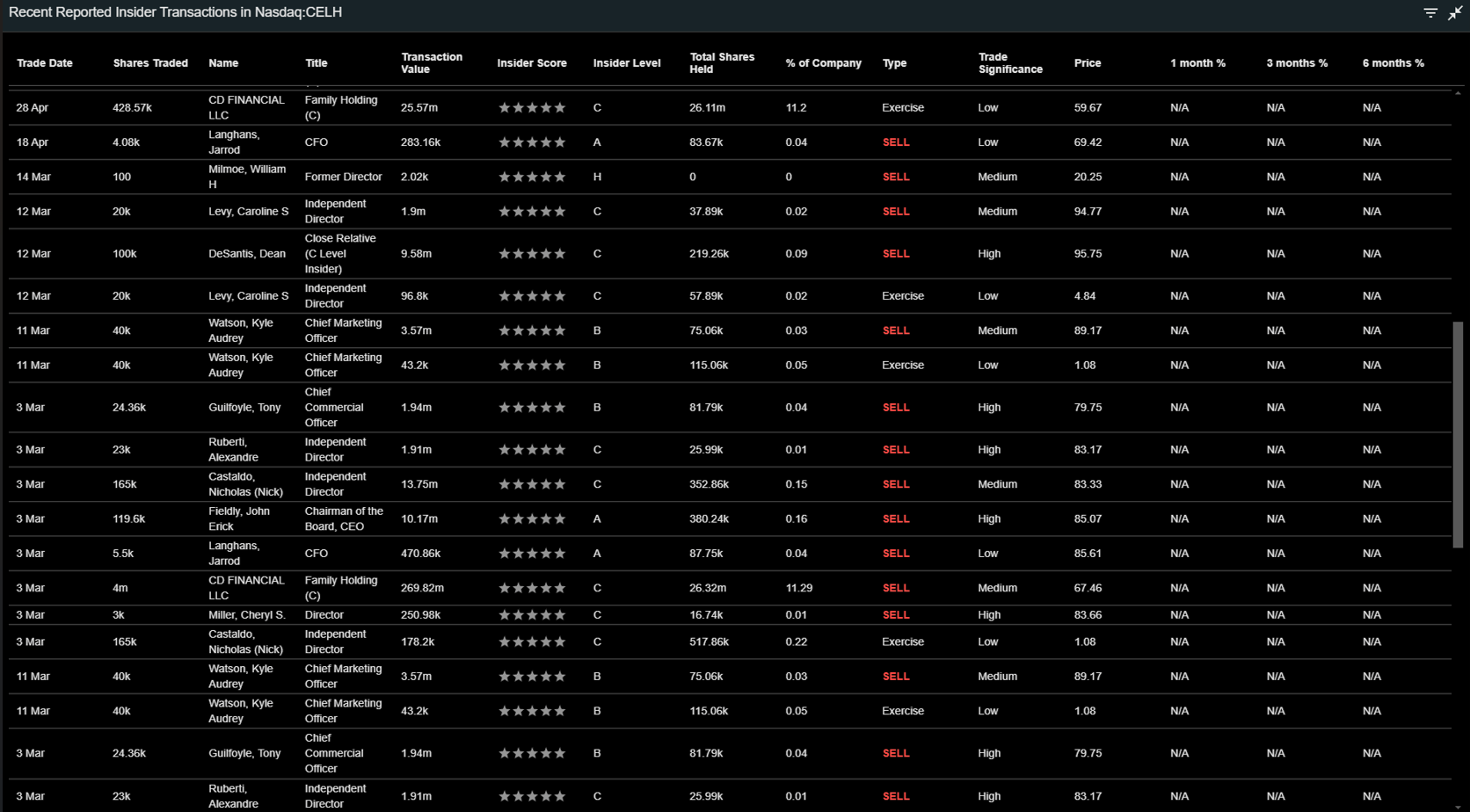

These seven executives have collectively sold 771,000 shares — through both direct ownership and by exercising options — in the year since Carl DeSantis’ death. Those sells have totaled $64 million.

Even John Fieldly – the company’s Chairman, CEO, and fearless leader – has sold $43.4 million worth of stock and options during the past year.

Many of Celsius’ other active and former directors have been selling shares as well.

None of the DeSantis family, the seven executives, or the Board of Directors have purchased a single share during the past year. They have all only been selling.

Collectively, Celsius’ insiders today own less than 2% of its outstanding shares.

With the company’s stock skyrocketing in recent years and with plenty of growth still on the horizon, wouldn’t they want to have more skin in the game?

This was the red flag that I discovered first and foremost. It smelled like something just wasn’t right…and is what led me to spend all day digging deeper.

Celsius’ Chief Commercial Officer Tony Guilfoyle is a ghost.

I don’t mean that he’s a haunting or supernatural being. But in terms of having any form of a digital presence, he’s pretty much invisible.

What does show up are a few pictures of Tony at red carpet events and with his celebrity sister Kimberly Guilfoyle. And Kimberly opens an entirely new can of worms.

Here is the exact wording of Celsius’ distribution agreement with Pepsi:

Though it is worded that the agreement will run through at least the year 2041, there doesn’t appear to be any penalty that Pepsi would be required to pay if it were to break the agreement for any reason “without cause”.

There’s certainly benefit and upside in this agreement for Pepsi. They have an 8.5% ownership stake in the company and are receiving $27.5 million from Celsius annually as a dividend for their preferred shares. They also got a seat on the Board of Directors, which they filled with Jim Lee. He’s their former Senior VP of PepsiCo Beverages in North America, who seems to be the right person for the job.

But I consider this to be a huge risk of customer concentration. Pepsi holds all of the cards here. It accounted for 59% of Celsius’ sales last year and also controls the distribution and the shelf-space relationship with retailers.

Furthermore, Celsius’ management seemed completely unaware that Pepsi would be placing $100 million to $120 million less in orders during the upcoming third quarter, as they destocked their existing inventory.

Here’s what CFO Jarrod Langhans rather confidently said during Celsius’ second quarter conference call on August 6th:

During the quarter, we publicly stated that the impact of the inventory movements during the middle of June was approximately $20 million to $30 million. As we closed the quarter, we saw a slight uptick in the days on hand, and as a result, the impact was at the lower end of that range.

They’re the one managing their inventory. So we’ll have to see where they end up where we are today. I think we’re in pretty good shape.

Yet less than one month later, it seems to have caught Langhams completely by surprise to find out that Pepsi would in fact be placing so much less in orders during the third quarter.

Isn’t Celsius gaining share on its rivals and growing the entire energy drink category? Why would Pepsi suddenly need to destock so significantly? I originally thought that it purposely overbought in order to fulfill demand. But this is a pretty massive delta. It’s seeming more likely that Celsius isn’t selling off the shelves as quickly as Pepsi was expecting. And it also feels like management’s claims of gaining market share are out-of-sync with Pepsi ordering significantly less product.

If Pepsi were to demand more favorable pricing or walk away from the agreement for any reason — perhaps due to brand damage, concerns about health issues, or even just fading interest from consumers — Celsius would lose all of that revenue and distribution.

These final two red flags aren’t flagrant fouls, yet they still caused me to lose confidence in Celsius as an investment.

Celsius’ world headquarters is listed as 2424 North Federal Highway, Boca Raton, Florida 33431.

That is an unmarked building, with no Celsius logo or branding out front. In addition to Google Maps, I similarly wasn’t able to find any branding present on the images of its HQ in an internet search. That strikes me as odd for a company that’s worth nearly $8 billion.

Furthermore, I also don’t have a ton of confidence in Celsius’ Board of Directors – which includes an advisor of a local pizzeria (Nick Castaldo), a distributor of art supplies (Damon DeSantis; Carl’s son), and a provider of marine products (Cheryl Miller).

Aside from Fieldly and Jim Lee from Pepsi, they don’t seem to have much experience in running publicly-traded companies in the beverage industry.

If all of the above weren’t enough, my final red flag is that consumer tastes are fickle and that consumer retail is difficult.

I don’t personally buy the claims that Celsius actually boosts your body’s metabolism. I do think that its 200 mg of caffeine speeds up your heart rate and gets your blood pumping faster. But that’s a far-cry from its claims of having thermogenic properties.

I believe Chief Marketing Officer Kyle Watson will similarly be fighting an uphill battle when it comes to convincing consumers that Celsius is differentiated from its competitors. The drink does have a nice taste and it offers a mid-afternoon pep. But the miracle-drug claims that are apparently supported by scientific studies feel like a stretch. I wish Celsius would stop citing them, as it’s damaging to its credibility.

Yet besides the brand and these claims, what does Celsius truly own?

After all:

And yet Celsius is spending 30% of revenues on sales & marketing every year. Including hefty amounts of stock-based compensation that’s immediately getting exercised for cash.

Sometimes it messes up on that marketing spend. In January 2023, it awarded rapper/influencer Flo Rida $82.6 million worth of royalties and equity for his early-stage promotions. That $82 million represented more than 30% of the company’s entire gross profit in the previous year.

I’ve started to get the feeling that Celsius’ entire business is primarily a marketing hustle. It doesn’t own any IP, any manufacturing equipment, or any long-term assets.

And while Pepsi showed up like a white knight and brought the company to profitability, its recent inventory destocking just proves that it’s going to do whatever is best for its own business and that Celsius’ management doesn’t have much visibility into what that might be. Things can change quickly in consumer retail, and that could similarly quickly burn Celsius and its shareholders.

I expect I will catch some heat for this sell recommendation. And I likely deserve it.

I should have discovered these red flags in my initial diligence, and that might have kept Celsius from ever finding its way onto our Best Buys Portfolio and our September Recommendation in the first place. For that, I am sorry.

But I also believe selling is the right thing to do. I’ve committed to always be transparent and objective in my analysis; which also means changing my mind if the situation demands it. If there’s any silver lining to this, it’s that doing this thorough level of research was enough to uncover the warning signs that weren’t obvious in the company’s earnings results, financial statements, or public-facing presentations.

There’s a bull case to be made that Celsius’ stock price will go up from here; perhaps even quite significantly. It is selling at an attractive valuation compared to its growth rates and I wouldn’t blame anyone for continuing to hold onto their shares. After all, Monster Beverage also exhibits several of these same red flags — such as questionable leadership credibility and concerns about health issues — and it has still turned out to be the best-performing stock of the past three decades. And it’s always possible that Pepsi just ends up buying Celsius outright and bringing the profit margins in-house.

But there’s also a strong bear case to be made that there’s a new energy drink waiting in the wings. One that increases your sex appeal, cheers for your favorite football team, and even does your taxes — and that Pepsi devotes its valuable retail shelf space to this new up-and-comer within a few years. If that were to happen, Celsius wouldn’t appear to have much left to offer to its shareholders.

In good conscience, I cannot keep this company on our scorecard after learning everything that I did yesterday. I recommend selling Celsius and will also be selling my personal holdings within the next 24 hours.