Coupang is Worth $19.25 Per Share, But With Hidden Upside. Here’s Why.

The base case of my Discounted Cash Flow predicts Coupang's stock is currently worth $19.25 per share. But like we saw this morning, it also has some excellent hidden optionality.

April 12, 2024

To see my previous Discounted Cash Flow for Rocket Lab, click here.

Update: Just this morning (April 12th), Coupang announced a 58% increase to the price of its WOW membership. This information has now been accounted for and the stock price target has been updated.

Anyone who’s invested in Amazon (Nasdaq: AMZN) already knows that e-commerce is a winner-take-most market.

Buyers want to be where the sellers are and vice-versa. This network effect leads to quasi-monopolies, where a single or a handful of companies reap the lion’s share of the traffic, volume, and profits.

We’ve seen this phenomena play out regionally all across the globe. Bezos’ Everything Store is dominating in North America. Alibaba (NYSE: BABA) and JD.com are a two-horse race in China. And MercadoLibre (Nasdaq: MELI) is muy populár in Latin America.

Yet one company who might still be off your online marketplace radar is Coupang (NYSE: CPNG), who is the e-commerce leader in South Korea. In addition to selling $24 billion per year of goods, it’s also the country’s third-largest employer (behind only Samsung and Hyundai).

Coupang has invested aggressively in logistical infrastructure in order to provide its shoppers with “Dawn Delivery”. You can place orders up until midnight and have them arrive on your doorstep by 7 AM the next morning. Similar to Amazon Prime, its “WOW” membership provides free shipping, unlimited returns, and other perks like digital content streaming and its grocery delivery.

Coupang’s rapid growth is exciting. But we also want to know that its hefty capital expenditures will eventually result in future cash flows. The company can use those cash flows for our benefit through shareholder-friendly capital allocation moves, such as dividends or share repurchases.

But growth-style investments in hot markets also sometimes fall into the Hype Cycle. The expectations get too high and the valuations get too frothy, which are the textbook recipe for lower forward returns.

It’s always a good idea for investors to stay grounded in reality. To objectively estimate a company’s future cash flows and to use them to determine a fair value for the stock.

So what’s a reasonable price for us to pay for Coupang’s shares today?

Introducing the Discounted Cash Flow Valuation

To answer that question, we need to bring in a useful new tool.

Doing so involves a discounted cash flow analysis. A DCF estimates future free cash flows — i.e. the cash that a company generates after paying all of its operational and capital costs — and then discounts them to the present day. The end result is a fair value, representing what that shares are worth for investors to pay to be the owners of those future free cash flows.

DCF models are the primary way that Wall Street firms set price targets for stocks. They’re not simple and are a huge time commitment to do properly. Here’s a quick look at the financial magic and voodoo that’s being run in the models.

This month I’ve set my sights on Coupang. Who certainly looks primed to generate sustainable profits in Korea for at least the next decade.

As before, I build my DCF models from scratch. I don’t look at other reports or price target estimates because I want to avoid any bias. My inputs are purposely conservative, to result in a price target that investors should be very comfortable in paying.

But as I mentioned in the title, using conservative assumptions will ultimately result in a lower price target. There are other drivers that, if they come to fruition, could provide significant additional upside.

So all of that said, let’s jump right to the punchline. Including today’s announcement of its price increase, I believe Coupang’s stock is worth $19.25 per share.

At today’s price of $21, Coupang appears fairly priced or perhaps is moderately overvalued. But as I’ll discuss a bit below, its recent acquisition of Farfetch could be a ‘hidden driver’ that could unlock value and drive the stock price higher.

And before we get into the trenches of my entire model, I’d like to quickly promote our 7investing service.

This article contains institutional-grade research, and it’s only possible to be published for free because of our generous paying subscribers. If you find value in this article, please consider joining 7investing for just $1 and getting similar research on all of our official stock market recommendations. Your 7investing membership also includes access to our Community Forum, where our advisor team and other investors are discussing stocks on a 24/7 basis.

Now, let’s get into the details of my Coupang DCF.

Inputs and Assumptions

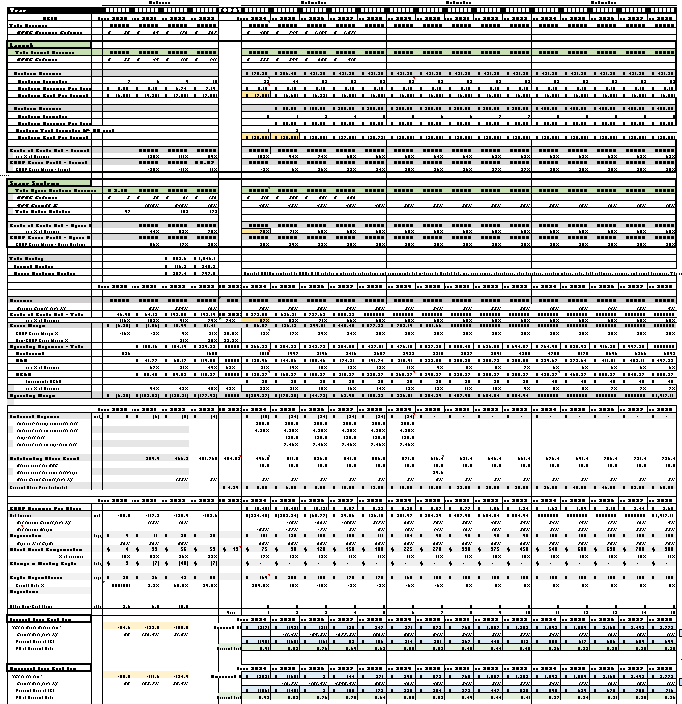

Revenues

As an online marketplace, Coupang derives revenue primarily from the goods it sells on its platform. And that’s a function of the total users, the total purchases, and the average purchases per user over time.

It recognizes its revenue in two segments: Product Commerce and Developing Offerings.

Product Commerce

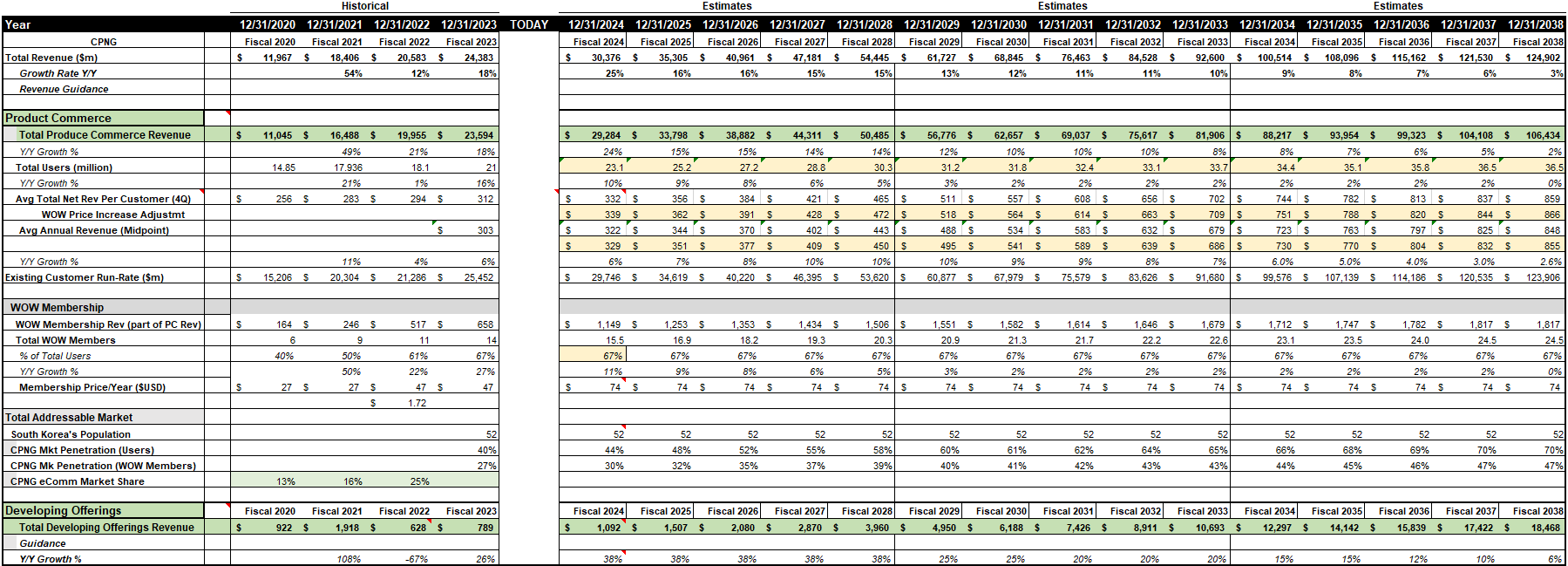

Product Commerce is 97% of the top line. The revenue represents the total value of the items sold, since Coupang takes ownership and then inventories from its merchants. This segment also includes revenue derived from merchants who pay Coupang to deliver orders using its logistics network (“Fulfillment and Logistics by Coupang”).

Coupang presently has 21 million total users who spent an average of $312 USD on the platform last quarter. 14 million of those users are WOW members, who pay an additional $47 per year [update: this was very recently increased by 58% on April 12th, from 4,990 to 7,890 won per month which is $74.26 USD per year] for the free shipping and the extra perks. The contribution from the membership fees is recognized as Product Commerce revenue and falls almost immediately to the bottom line. Coupang last raised the price of its WOW membership by 72% in 2022 and still increased its membership by 62% that year.

Here are the specific expectations and inputs for Product Commerce that I’ve used in my DCF model:

Coupang did $23.6 billion in Product Commerce revenue last year, with 21 million users spending an average of $312 in the fourth quarter.

Korea’s inflation rate is 2.6% and the average wage per full-time employee is around $3,000 USD per month.

CEO Bom Kim has reported in the most recent conference call that “every one of our [customer] cohorts is growing over 15%, even our oldest cohorts.” I have thus modeled for the spend per user for the existing 21 million users to increase 15% in 2024 and in future years.

In addition to the core user base, Coupang is also adding new users at around 16% per year. I’ve modeled for 10% user growth in 2024, which slows down over time. I also estimate that new users spend just 20% of existing users during their first year. [I have back-checked this math, based on Coupang’s membership growth and overall avg rev/customer in 2023. 20% is the right number to use.]

The combination of the above allows me to estimate a blended average total quarterly revenue per user. This reported metric refers to all revenues; not just Product Commerce transactions.

I estimated $322 quarterly net revenue per user in 2024. HOWEVER, Coupang’s price increase to 7,890 won per month will directly boost this number. $74.26 USD per year is around $7 USD per quarter higher than the previous $47 USD per year. I am adding the price increase to the average total revenue per user, and now estimating $329 quarter ARPU in 2024.

Overall, I expect ARPU rises to $351 in 2025 and gradually increases all the way up to $855 per quarter by the year 2038. This is a very conservative assumption, especially since we’ll see a 2.6% increase on price alone and likely a 4x-5x increase in volume after 5 years.

WOW membership remains at $74.26 USD per year for all future years. This is a conservative assumption, as we just saw this morning that Coupang isn’t shy about raising its membership prices.

I’m modeling 23 million users and 15.5 million WOW members in 2024, rising to 30.6m and 20.5m in 2029 and eventually 36.6m and 24.5m in 2038. Keeping the WOW membership constant at around two-thirds of total users.

Overall, the above bring me to estimate $30.4 billion USD in total revenue in 2024, which rises to $61.7 billion in 2029, $101 billion in 2034, and $125 billion in 2038.

I’m expecting the majority of this total revenue estimate to continue to come from Product Commerce. $29.3b in Product Commerce in 2024, $57b in 2029, $88b in 2034, and $106b in 2038.

Developing Offerings

The Developing Offerings segment are tangential services such as prepared food delivery (Coupang Eats), its standalone digital streaming service (Coupang Play) or its newly-launched marketplace and logistics in Taiwan. As the name suggests, they are still very early stage programs that Coupang is beta-testing to see if there’s anything worth pursuing.

Developing Offerings are “growing twice as fast as the core retail business.” Its most recent fourth quarter revenue of $273 million was up 105% over last year.

As mentioned above, Coupang’s “Average Revenue Per Customer” relates to all segments — which includes both the retail sales and the developing offerings.

I’ve split it accordingly, to keep the growth rate of Developing consistently around 2X that of the core platform.

I’m expecting for 38% annual growth for this division through 2028, mainly due to its vast investment of $2.2 billion into warehouses in Taiwan.

I’m modeling $1.1b of Developing Offerings revenue in 2024, $5b in 2029, $12b in 2034, and $18b in 2038.

Coupang’s revenue forecast

Costs of Goods Sold

Coupang is aggressively investing in its logistical footprint, especially in Taiwan where it had the most-downloaded app in the country last year. It should continue to see improvements in logistical efficiency and margin expansion.

Coupang’s gross margin is largely a function of its cost to buy and inventory the products, and then to pay the logistics costs to deliver them (including driver salaries).

They have specifically mentioned automation and AI as initiatives to help them expand gross margins. Especially in the purchasing and delivery of perishable vegetables, as well as getting the most deliveries per driver per hour possible. They’re also adding extremely high-margin ad revenue to the top line. And Eats only costs a fixed amount per delivery (which was $1.70 USD last year), since they’re just paying the contract drivers and not investing in their own trucks or gas.

All of the above have allowed Coupang to consistently grow its revenues faster than its associated Costs of Goods Sold. It recognized an impressive 250 basis points of gross margin improvement in 2023. I expect gross margin to continue to expand, but at a much more conservative rate going forward.

JD.com in China has a similar model — i.e. holding the inventory and capturing the logistics efficiencies. And even though JD is a very mature company, its gross margin of 14% is almost half of Coupang’s 25.4% gross margin.

That means logistics efficiencies are a big deal! I estimate gross margin will slowly expand, from 28% in 2024 (200 basis points higher, post price increase, than management’s previously stated goal of 26%) to 30% in 2029 and then 31% by 2038. This is a very conservative assumption that Coupang could very well exceed.

Coupang’s COGS forecast

Operating Expenses

Operating expenses and margins are tricky, since Coupang doesn’t break out its individual line items for Sales General & Administrative, Research & Development, or Overhead.

What we do have reported is Adjusted EBITDA — which is operating income with depreciation, amortization, and stock-based compensation added back. We can use that as a guide to model operating profits.

Coupang reported that its core Product Commerce segment generated a 7.1% adjusted EBITDA margin in 2023. I’ve extended that into 2024 and also into future years (though it will likely increase). Product Commerce generates a $4 billion EBITDA profit by 2029, $6b by 2034, and $7.5b by 2038.

Developing Offerings will reportedly record “a $650m Adjusted EBITDA loss in 2024”. I am modeling for those to decline over time, as Developing Offerings becomes EBITDA break-even by 2029.

It eventually generates a $1 billion EBITDA profit by 2034 and $2 billion by 2038.

Furthermore, I estimate Operating Expenses will roughly follow COGS growth and be aggressive during the investment phase of the next five years. Coupang has committed $2.2 billion to its logistics in Korea and another $1.5 billion+ for Taiwan. That will show in the CapEx line item and will similarly affect OpEx.

Op profit was $473m in 2023. I estimate $1.3 billion in 2024, $3.9b by 2029, $5.8b by 2033, and $8.7b by 2038.

Op margin increases from 1.9% in 2023 to 4.4% in 2024 to 6.3% in 2033 to 7.0% in 2038.

As a sanity check, MercadoLibre’s GAAP-reported op margin was 9.8% in 2022 and 12.6% in 2023. So my estimate for Coupang errs on the side of being conservative.

Adjusted EBITDA margin increases from 4.4% in 2023 to 4.7% in 2024 and 7.7% in 2038.

Coupang’s operating profit forecast

Debt, Interest Expense, Earnings Per Share

Coupang’s balance sheet is actually quite strong right now. It has $5.2 billion USD in cash, with only $1 billion in total debt (including short-term holdings; but excluding its operating least commitments).

Between the $550 million in CapEx it’s spending in Korea and then the additional $400 million in Taiwan, I estimate they’ll spend $4.8b in total CapEx during the next 5 years. They’ll likely also require additional financing in order to fund their working capital, since they own their inventory of everything sold on the platform.

Coupang has a credit revolver that offers up to $1 billion of additional financing. I’m forecasting they’ll take $500 million of that in 2025 and another $500 million in 2026, then have it fully-repaid by 2028.

Coupang has done a bit of financing through equity raises, but they’ve done right by us as shareholders. Dilution has averaged just 1.3% annually during the past three years — even during the company’s expansion phase. I extend that same 1.3% per year will continue, ultimately resulting in a share count of 2.2 billion by 2038.

The company really did a fantastic job at raising $4.8 billion in its 2021 initial public offering. It timed the market perfectly, and now is financially in really good shape.

Coupang’s EPS forecast

Capital Expenditures, Depreciation, and Stock Based Compensation

I’ve also made quite a few capital expenditure forecasts and non-cash adjustments:

Fulfillment centers and equipment generally have a 15-year useful life. I’ve tied depreciation to Net PP&E and CapEx.

Depreciation will converge to CapEx in the later years, as Coupang begins spending primarily on maintenance rather than on growth.

CapEx has been explicitly stated by management to be $2.2 billion through fiscal 2027 for investment in Korea + $400 million/year in Taiwan.

I’m modeling $950m of CapEx through 2027, increasing to $1b in 2028, and then gradually walking it down to $500 million/year by 2036.

As a sanity check, MELI spent $509m on CapEx last year. The numbers check-out.

I looked at the proxy and it looks like Coupang’s executives have a reasonable equity compensation plan that won’t result in massive dilution. I’m therefore tying SBC growth to the growth in overall headcount, which grows 12% in 2024 but slows down a bit in later years. SBC never accounts for more than 1.3% of total revenue or 25% of Adjusted EBITDA.

Working capital is tricky due to the stockpiling of inventory. Some years it loads up and other years it works through it. I’m having the two offset one another and am assuming a zero change in working capital needs throughout the DCF.

Acquisitions are also a trump card. We know Coupang paid $500 million for Farfetch this year, but we’re still unclear on the impact it will have on financials.

For the time being, I’m baking Farfetch’s revenues and growth entirely into my expected growth rate of the core platform. This is a conservative assumption that I’ll likely boost in future versions.

Coupang has a defined-benefit pension that is overfunded and a reductions in its estimated discount rate have provided a net cash benefit in recent years. It’s also made a few gains on its short-term investment securities. I’m zeroing out the pension benefit, but I think it’s reasonable to assume that the company can continue to get a 2-3% return on its $5 billion of cash in the bank. So I’ll continue to recognize a $150 million operating gain in each year of the forecast.

I’m also capitalizing the operating lease, which gives it right-of-use for several of its facilities without owning them outright. So I’m recognizing the current value of the liability as a debt, but also adding back the $450 million per year in expenses.

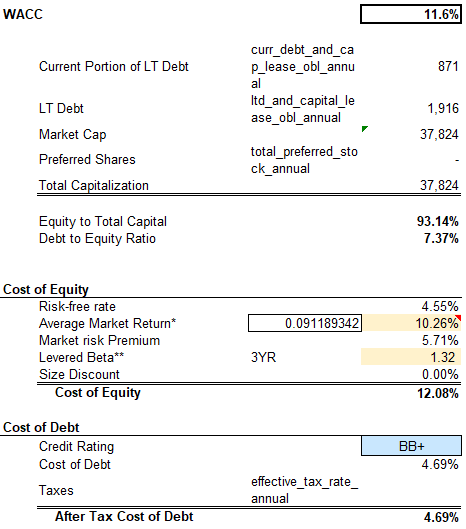

Debt and the Weighted Average Cost of Capital

Here are the inputs I’ve used for Coupang’s long-term debt and weighted-average cost of capital.

I’ve capitalized all operating leases

I’m assuming $1 billion USD of additional long-term debt in 2025-2026, which gets fully repaid by 2028

The company’s cost of equity of 12.1%, which is based on a 10.26% average market return and Coupang’s Beta of 1.32

Coupang’s cost of debt of 4.69% based on a BB+ credit rating and its use of assets as collateral

Coupang’s overall WACC is 11.6%

Coupang’s weighted average cost of capital

Other Key Assumptions

Recapping much of what I’ve mentioned above, here are a few of the key assumptions of this model:

$29b of Product Commerce revenue in 2024, $57b in 2029, $87b in 2034, and $106b in 2038. Which is a growth rate of 24% in 2024, 12% in 2029, and then just the rate of inflation in the terminal year.

$1.1b of Developing Offerings revenue in 2024, $5b in 2029, $12b in 2034, and $18b in 2038. 38% growth rate in 2024, 25% in 2029, and tapering off from there.

Gross margin will slowly expand from 28% in 2024 to 30% in 2029 and then 31% by 2038.

Operating expenses will roughly follow COGS growth and be aggressive during the investment phase of the next five years. Op margin increases from 1.9% in 2023 to 4.4% in 2024 to 6.3% in 2033 to 7.0% in 2038.

Adjusted EBITDA margin increases from 4.4% in 2023 to 4.7% in 2024 and 7.7% in 2038.

Shareholder dilution of 1.3% per year. 2.2b shares by 2038.

Maintaining a few of the non-cash benefits and capitalizing the operating lease.

Assuming the benefits of the $500m Farfetch acquisition are baked into core platform growth.

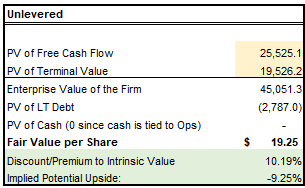

WACC of 11.6%. $2.78b present value of liabilities. 2.2b outstanding share basis. 3% terminal growth rate.

I used a 15 year growth window and assumed a terminal growth rate of 3% for the cash flows beyond 2038. I then discounted all of those future cash flow back to the present.

Coupang’s free cash flow forecast

So What’s Coupang Worth?

So now that we’ve gone through all of the inputs, let’s circle back to that punchline. I estimate Coupang’s present equity value is worth $19.25 per share.This represents the fair value of what Coupang’s shares are worth today.

Coupang’s current stock price of around $21 appears to be reasonable valued, if not a bit overvalued.

But let’s also remember that I’m using some very conservative assumptions. Coupang has historically executed much better than this model is currently anticipating. It also includes very limited contribution from Farfetch, which could have significant upside if Coupang figures out how to integrate it.

Even better, we just received news this morning the news of Coupang’s price increase for its WOW membership. That alone made — by my estimates — the stock worth 16% more than it was yesterday. Future price increases would also boost the price target.

But this is just the beginning. DCFs evolve over time, and I’ll be digging deeper into the impact of logistical efficiency, Farfetch’s contribution, and the membership fee increase in version 2.0 of the model.

I’ll be sharing all of those on our 7investing Community Forum. And I would love to invite you to join in on the conversation.

Coupang’s fair value

Want to discuss Simon’s assumptions on Coupang directly with him and with other investors?

“Thanks for doing this. So much work goes into these models, that this kind of financial calculus on individual stocks is worth the price of admission by itself.”

“Thanks a lot for working through this publicly, really an excellent exercise.”

“Thanks a lot, Simon. I feel like some of your assumptions are quite conservative, and it is astounding that you get to such a crazy upside anyway. What really makes me believe that the upside is possible is that they keep performing and delivering on their promises.”

“Thanks for the modeling!”

“Thanks for the hard-work, 7innovator! Would be interesting to see if this impacts the conviction rating..”

These are posts in our Community Forum posts from actual 7investing members. Click here to join 7investing’s Community Forum today!